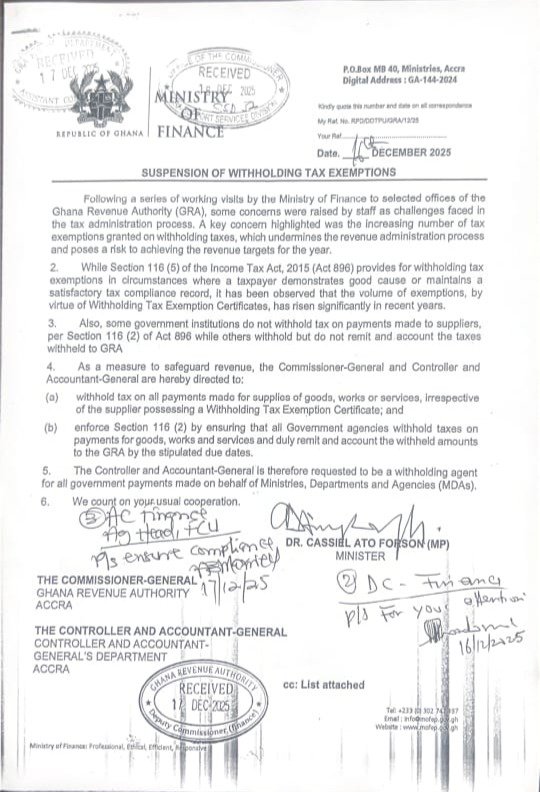

The Minister of Finance has directed the Ghana Revenue Authority (GRA) and the Controller and Accountant-General to ensure that tax is withheld on payments made by Ministries, Departments and Agencies. This directive was issued on 16 December 2025 and is already in force. The GRA has implemented this directive by excluding payments by government agencies from the new withholding tax exemptions issued to qualifying taxpayers.

According to the Minister, this directive is necessary because some staff members of the GRA expressed concerns about the high number of exemptions. These staff members say that there is a risk to meeting the GRA’s revenue target due to the large volume of exemptions granted.

Below is our opinion on this development.

What is withholding tax?

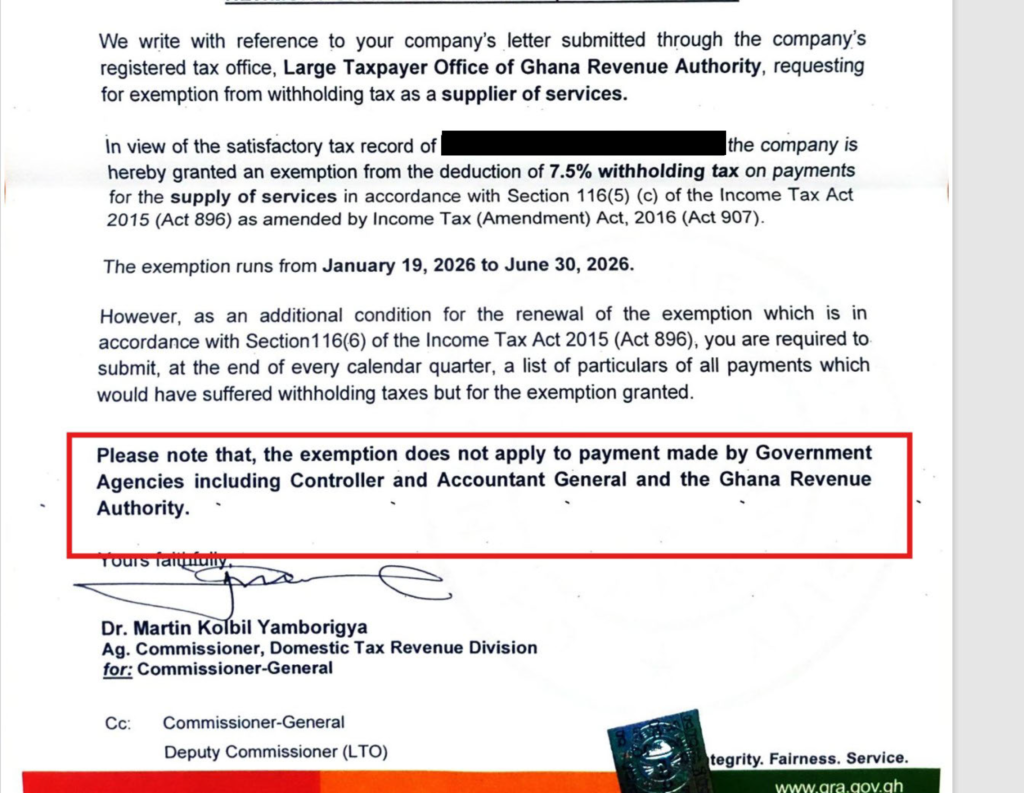

Section 116(5)(c) of the Income Tax Act, 2015 (Act 896) empowers the Commissioner-General (CG) of the GRA to exempt some taxpayers from tax being withheld on their income. The income is not exempt from tax. It is only the advance tax that is not required. The GRA goes through a lot of reviews before granting any withholding exemption. The detailed procedures can be found on pages 16-19 of the Practice Note on Withholding. Further, the exemption is typically granted twice a year, first period ending in June and the other ending in December. The exemption is renewed upon meeting all the specified conditions.

Does withholding tax exemption really pose any risk to Government revenue?

Though this is the concern expressed to the Minister by the GRA staff, it is difficult to fully appreciate this point. Assuming the withholding mechanism is the only way taxes are paid during the year, this concern would have carried a lot of weight. The fact is that every person who earns business or investment income is required to pay quarterly taxes. By the end of the first quarter of the taxpayer’s accounting year, they are required to file an estimate of their income tax for the year. That estimated annual tax is then divided into four and paid quarterly. So, for those whose accounting years end in December, by 31st March, they should have filed the 2026 annual tax estimate and paid the first quarter taxes.

This quarterly tax system is regulated by sections 121-123 of Act 896. The cash amount to pay for each quarter is determined by a formula. The formula is the total estimated annual tax minus the total tax paid so far, all divided by the remaining quarters. The total tax paid includes previous payments made in cash and taxes withheld. This means that for a person who is exempt from withholding taxes, their quarterly taxes will be paid wholly in cash since they have no tax withheld. For a person who is not exempt, any cash they pay will be reduced by the tax withheld. For instance, if the quarterly tax to be paid is GHS100 and tax of GHS30 was withheld, the taxpayer will end up paying the difference of GHS70. Assuming no tax was withheld due to the exemption, the taxpayer would pay the full GHS100. So, with or without withholding, the revenue administration process is not undermined.

Additionally, the GRA has enough tools to deal with anyone not paying the correct tax. Severe sanctions exist for anyone who fails to pay at least 90% of their taxes during the relevant year. People who even pay their taxes late are punished with hefty sanctions. Rather than relying on withholding taxes to meet revenue targets, staff of the GRA should rather ensure those who deserve the full exemptions honour their tax obligations.

Conclusion

Though this directive only affects payments from the Government, the basis for such a decision is questionable. Persons who enjoy withholding tax exemptions are known to the GRA. Those in tax-paying positions are expected to file their estimated taxes and make quarterly payments. Taxpayers who make losses are not part of this discussion because due to their losses, they should not be paying any tax, else they will simply come back for refund after using their capital to pay taxes. Given the recent cut in the allocation to the refund account, refunds should not be unnecessarily created. In our view, based on the rationale given for the directive, the directive is unfortunate.