The Court of Appeal recently reversed a ruling of the High Court. The consequence of the decision from the Court of Appeal is serious and shakes one of the pillars of the VAT system in Ghana. Not only does the judgment offend an express provision of the law, it sins against other decisions of the Supreme Court on procedural grounds. This article reviews the judgment and discusses serious issues with the decision.

Background

Agility Distribution Parks Limited believed that the Ghana Revenue Authority (GRA) was illegally refusing to refund its excess tax payments. The GRA owed GHS200,112.45 as excess company income tax. Additionally, the GRA owed GHS12,197,887.61 as excess VAT payment. Agility requested a refund of these tax overpayments, relying on the Revenue Administration Act, 2016 (Act 915).

The GRA refused to refund the excess taxes. Agility wrote to the GRA on 9th December 2020 to demand the refund, but the GRA didn’t respond. Agility treated the GRA’s silence as a refusal and filed a judicial review application at the High Court for an order of mandamus. A mandamus order commands public officials to perform their duties.

At the High Court, Agility fully relied on Act 915 as the applicable law relating to refunds. It rejected any attempt by the GRA to rely on section 50 of the Value Added Tax Act, 2013 (Act 870). Specifically, it said the provisions in section 50 of Act 870 which dealt with how to treat overpayments of VAT do not apply because they have been impliedly repealed by Act 915. Conversely, the GRA relied on section 50(1)(a) of Act 870 to argue that any overpayment of VAT arising from excess input over output must be credited to the taxpayer. So, no refund is due under Act 870. Further, Act 915 doesn’t even apply because it is a general law applying to all tax types while Act 870 is a specific law affecting only VAT and hence is the only applicable law.

The High Court agreed with the GRA’s argument relating to the principle that a specific law must prevail over a general law whenever there is a conflict. The High Court failed to specifically address the excess company income tax payments. Dissatisfied with High Court’s ruling, Agility appealed.

Procedural error

It is surprising that the Court of Appeal went into the merits of the appeal. This is because the procedure adopted by Agility offends the law and so the High Court didn’t even have jurisdiction to entertain the matter in the first place. The correct procedure was for Agility to treat the GRA’s silence or refusal as a tax decision and then to follow the dispute resolution procedure in Act 915. Ghanaian courts have repeatedly held that based on the current state of the law, a person dissatisfied with a tax decision cannot invoke the supervisory jurisdiction of the High Court but must invoke its appellate jurisdiction.

Specifically, on this matter of refunds, even the Supreme Court weighed in and said the established dispute resolution mechanism must be invoked rather than applying for judicial review. We may forgive the High Court for even looking at the merits of the case when the case started in 2021. The Supreme Court’s ruling came in 2022. We however cannot forgive the Court of Appeal. By going into the merits of the case which invoked the wrong jurisdiction of the High Court, the Court of Appeal ignored statutory procedural requirements and binding precedents.

The case of Republic v High Court Ex Parte: Afia African Village Limited, Interested party: Commissioner-General, which was decided in 2022, is binding on the Court of Appeal. The Applicant in that case also demanded a refund of taxes and the GRA refused. It also applied for mandamus, a judicial review remedy at the High Court. The High Court refused the application on the basis that the procedure for dealing with tax disputes was not followed and so the High Court did not have jurisdiction to grant the application. The Applicant then sought a further review of the High Court’s ruling at the Supreme Court claiming the High Court committed an error in its ruling. On the question of whether the High Court had jurisdiction to entertain an application for mandamus where the Applicant had not exhausted the statutory dispute resolution procedures under the Revenue Administration Act, 2016 (Act 915), the Supreme Court said

It is thus evident that the applicant had not commenced, not even talk of having exhausted the procedure provided under sections 41(1) and (2)(b), 42 and 44 of the Revenue Administration Act, 2016 as amended by Act 1029 of 2020 before filing the application for an order of mandamus in the High Court under Article 141 of the Constitution, 1992, the Courts Act, Act 459 and Order 55 of C. I . 47.

In this instance, the High Court has no jurisdiction to have entertained the application for mandamus because its jurisdiction was prematurely invoked by the applicant. The applicant had all the time at her disposal to have fulfilled these apparent conditions or legal steps before embarking on mandamus before the High Court but rather sat down and allowed time to elapse …

The law has made adequate provisions for refunds due under the tax laws but the applicant in the instant case refused to abide by them. The applicant’s resort to mandamus is premature and very wrong in law as the interested party was not under statute to refund same. The trial High Court judge was right in dismissing same on procedural grounds.

Before the current Court of Appeal decision, the position of the law, as clarified by the Supreme Court, was that whenever a taxpayer demanded tax refund and the GRA refused or remained silent, that response from the GRA was a tax decision. Tax decisions must be challenged using the procedure in Act 915. For details on this procedure, see this article. When taxpayers skip that procedure and invoke the High Court’s jurisdiction by way of writ or application, the High Court wouldn’t have the jurisdiction to deal with the process before it.

With this new judgment, the Court of Appeal has endorsed a procedure that the Supreme Court has frowned upon and clarified as unlawful. It is even troubling that the Court of Appeal itself didn’t check if it had jurisdiction in the matter especially when it was dealing with an appeal. Appeals are done by rehearing the matter. It didn’t discuss whether it considered the GRA’s response as a tax decision or how the Supreme Court’s binding decision concerns this case. So now, we have two different positions on this issue. The Supreme Court requires the correct procedure of objection and appeal to apply for refunds while the Court of Appeal does not require it.

Substantive problems with the Court of Appeal’s judgment

Assuming the proper jurisdiction of the High Court had been invoked, there are serious issues with the judgment. At the High Court, Agility focused on arguing that section 50(1)(a) of Act 870 had been impliedly repealed by Act 915. That argument depended on the fact that Act 915 came in 2017 and is newer than Act 870, a 2014 law.

At the Court of Appeal, it repeated that argument but found a new argument. This new argument is that although Agility doesn’t accept that Act 870 applies to refunds and excess payments any longer, even if Act 870 must apply, the High Court made a mistake in not looking at sections 50(3) to 50(9) of Act 870. Indeed, this is the argument that convinced the Court of Appeal. The Court of Appeal rejected the High Court’s ruling that there was a conflict between Act 870 and Act 915 regarding how to treat overpayments.

The High Court relied on section 50(1)(a) of Act 870 after resolving the conflict in favour of Act 870. The Court of Appeal however didn’t see any conflict. It also didn’t see any reason to rely on Act 915. It said within section 50, there are enough provisions to justify a refund. So, essentially, it agreed with the High Court that it is Act 870 that must apply contrary to what Agility had been arguing.

Where it disagreed with the High Court was which of the subsections of section 50 applies to Agility. It said,

30. Agreeing with the trial court that the relevant law applicable is the VAT Act, Act 870, in dealing with the payment of the excess VAT tax that the Respondent clearly admits have been paid in respect of VAT in the sum of Ghc12,197,887.61. The question flowing from that finding and worth dealing with is whether it was right for the Respondent to have treated the VAT excess tax payment in the sum of GHS12,197.887.61 credited to Appellant in accordance with section 50(1) of Act 870, instead of the application of subsection 50(3) to (7) of the VAT Act?

The majority of the Court of Appeal correctly identified that there are two streams of refunds or dealing with overpayments in section 50 of Act 870. The first stream covers sections 50(1) to (2) while the other stream covers sections 50(3) to (9). The Court of Appeal said,

33. Section 50(3)-(9) stands on its own which provides a different incident for tax refund other than subsections (1) and (2), which the Respondent gleefully sought [refuge]. For the section 50(3) notes that subject to section 45, where the amount of tax paid by a person, other than in the circumstances specified in subsections (1) and (2), was in excess of the amount properly subject to tax under this Act, the amount of the excess shall be treated in the manner provided for under subsection (5) to (9).

The Court of Appeal itself identified that the two streams do not mix. The second stream only applies to items that the first stream does not apply. This is shown by the expression ‘other than‘ as used in section 50(3) of Act 870.

36. What section 50(3) of Act 870, implies is that for section 50(3)-( 9) to be applicable it should not be one that falls under subsections (1) and (2) and it must also not be one that comes within section 45 of Act 870. As the claim by Appellant was not one attributable to exports, it does not fall under sub section (1) and (2).

The conclusion that section 50(1) to (2) applies to exports is where we have concerns. The lead judgment does not explain how it arrived at this conclusion, but the concurring judgment does. That opinion says,

[65] The combined effect of section 50(1) and (2) is that if an overpayment of tax is arising from excess input VAT, that excess input VAT is credited to the taxable person and the taxable person can only claim a refund upon application within a. minimum of three months if the excess is attributable to exports and the taxable person exports at least 25% of its total supplies with the total export proceeds having been repatriated to Ghana.

[66] Importantly, reading section 50(1) as a whole, in a conjunctive and not a disjunctive manner, the following must be present:

– There must be more input tax than output tax to have a credit

– The excess must be attributable to exports

– The exports must represent about 25% of the proceeds of the taxable person

– The proceeds should have been repatriated to Ghana.

Review of the judgment

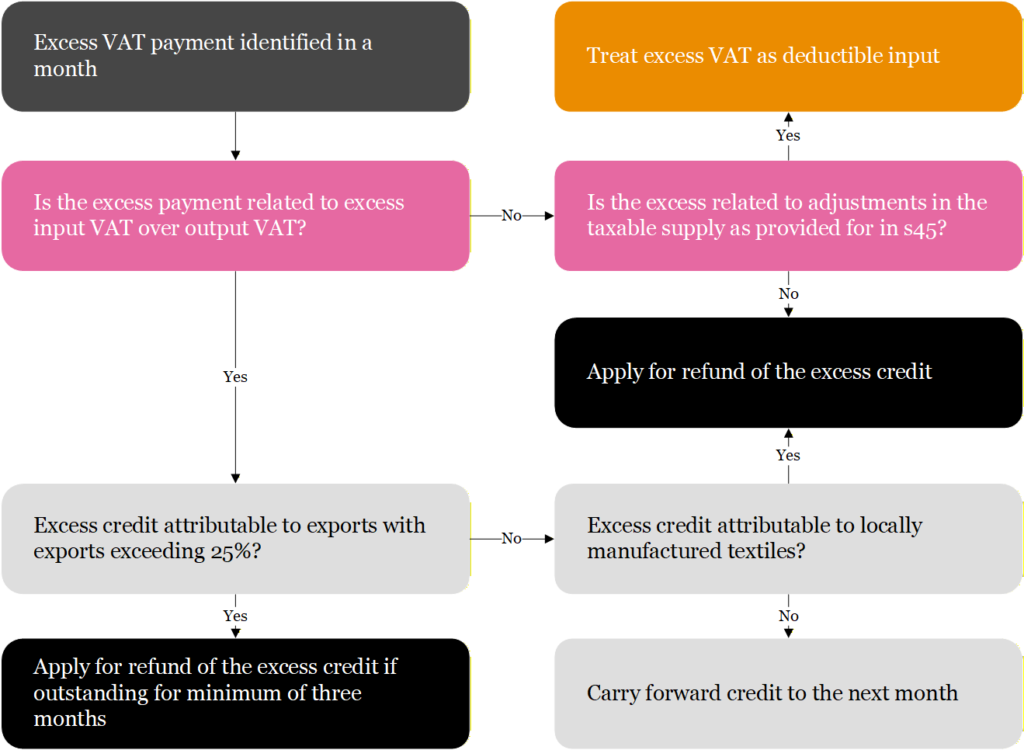

The amount of VAT payable in a month is captured in section 47(1) of Act 870. This provision says the amount to be paid to the GRA is the excess of output VAT over deductible input VAT. That is, a taxpayer only makes a payment when its output VAT exceeds the input deduction it is allowed. What happens if the reverse happens? Section 47(2) says when the deductible input VAT rather exceeds the output VAT for the month, we must go to section 50 of Act 870 to deal with the excess.

In the original text of Act 870, the only condition for which excess input VAT could be refunded related to exporters. In 2018, an amendment was introduced to expand the list such that the full text of section 50(1) now reads,

50. (1) Where the amount of input tax which is deductible exceeds the amount of output tax due in respect of the tax period,

(a) the excess amount shall be credited by the Commissioner- General to the taxable person, and(b) in the case of the portion of the excess attributable to exports, the Commissioner-General may refund the excess credit to the taxable person where that person’s exports exceed twenty five per cent of the total supplies within the tax period and the total export proceeds have been repatriated by the importers’ banks to the taxable person’s authorised dealer banks in the country, and

(c) in the case of the excess credit directly attributable to locally manufactured textiles subject to zero-rate as provided in the Second Schedule, the Commissioner-General may refund the excess credit attributable to that period upon the receipt of an application for refund of the excess credit. [Inserted by Value Added Tax (Amendment) (No. 2) Act, 2018 (Act 980)]

In our view, the Court of Appeal’s wrong interpretation can be traced to how it applied the conjunctive word ‘and‘ that is between section 50(1)(a) and (b). We agree that this is a conjunction and both (a) and (b) must be read together. However, because of the use of a conditional statement in (b), the provision in (b) must stand on its own and only applies if the conditions there have been met. The proper interpretation is that based on section 50(1)(a), anytime a taxpayer’s deductible input VAT exceeds its output VAT, the GRA must credit that input VAT to the person. After crediting the input, if the taxpayer is an exporter then section 50(1)(b) and 50(2) may apply.

The use of the expression, ‘in the case of‘ is a drafting style that simply specifies a condition. This condition in section 50(1)(b) has no effect on section 50(1)(a). Since both (a) and (b) must be read conjunctively, effect must be given to (a) at all times since there is no condition there. After applying (a), (b) must also apply. Section 50(1)(b) will only have effect when the condition is met. For an exporter, the conjunction means that after applying (a) and crediting the excess, once the conditions in (b) have been met, they can proceed to apply for refund if the condition in section 50(2) is also met. For non-exporters, since they do not meet the condition in (b), they are limited to (a). So, it is not the case that the entire section 50(1) relates to exporters.

One will notice that section 50(1)(a) is the only provision that does not contain any condition. It is a general rule that applies to any person with excess input VAT. Section 50(1)(b) to (c) contain conditional statements that apply to specific situations. Those are exceptions to the general rule in section 50(1)(a). So, any taxpayer that has input VAT and does not fall within any of the exceptions must carry forward the excess input VAT.

To confirm this interpretation, the Court of Appeal could have relied on the Value Added Tax Act, 1998 (Act 546), which was repealed and replaced by Act 870. Section 25 of Act 546 said

(1) Where the amount of input tax which is deductible exceeds the amount of output tax due in respect of the accounting period, the excess amount shall be credited by the Commissioner to the taxable person; except that in the case of

(a) exports, where the Commissioner may refund the excess credit to the taxable person where that persons exports exceed 25% of the total supplies within the accounting period and the total export proceeds have been repatriated by the importers’ banks to the exporters’ authorised dealer banks in Ghana, and

(b) the supplies specified in items 2 and 3 of Schedule 2 to this Act where the Commissioner may refund the excess credit to the taxable person.

Act 546 said the same thing that Act 870 also said. The only times that refund existed under section 25(1) of Act 546 were when exporters were involved and specific supplies were made. At all other times, the excess input VAT was credited to the taxpayer. This is the position that was maintained in Act 870. Indeed, section 50(13) of Act 870 was clear that

Except as otherwise provided in this section, a credit under subsection (1) shall be carried forward to the next tax period.

The Court of Appeal’s interpretation makes the provision above on carrying forward credits meaningless. This is because under this interpretation, every credit is available to be refunded under section 50. Qualified exporters got their refunds through section 50(1) and (2), and everyone else got theirs through section 50(3) to (9). If everything is refunded, what gets to be carried forward? Is it the case the exporters had more stringent rules such that if they do not meet the conditions in section 50(1)(b) then they must carry forward credits while everyone else was entitled to a refund? We don’t think so. This provision is clear that any taxpayer to whom section 50(1)(a) applies with no exception regarding a refund must carry the credit forward.

Section 50(3)-(9) deal with overpayments that are not related to excess input over output. For instance, when a taxpayer is making payment to the GRA and accidentally overpays, section 50(3) to (9) will handle this and require a refund. That is, instead of paying VAT of GHS5,000 for the month as disclosed on the return, the taxpayer accidentally pays GHS50,000. The excess of GHS45,000 is not an adjustment to the taxable supply to be handled by section 45. It is not a matter relating to excess input VAT. So, it qualifies under section 50(3) to (9) for a refund. Another situation is where the taxpayer’s VAT registration is cancelled by the GRA. If at the time of the cancellation, the person has been carrying forward credits, the person may apply for refund. This is covered in section 50(8).

Though the same provisions are in the new VAT law, the Value Added Tax Act, 2025 (Act 1151), the disjunctive word ‘or’ is used in section 53(1). Despite this, there is the danger that this decision can be applied even now.

Conclusion

The Court of Appeal’s decision creates confusion in the VAT system in Ghana. Since 1998, the law and practice have been that excess input VAT credit is carried forward and not refunded. Refunds are restricted to specific situations. With this new decision, taxpayers no longer have to carry forward any excess input VAT. If this decision is allowed to stand, the GRA will be overwhelmed with applications for refund because similar provisions are in the new VAT Act.

In our view, the decision is erroneous as it misinterprets section 50(1). The conjunction there was applied without considering the conditional statement in section 50(1)(b). We hope the GRA will appeal this decision and bring these issues before the Supreme Court.

Well written and provides ample context even to those without a legal background to appreciate the two levels at which the Appeals Court erred. Thank you for this insightful analysis

Thank you Edwin